The Death of Lifetime ISAs is On Its Way

Published / Last Updated on 30/06/2025

The Treasury Select Committee has today released its report on the effectiveness and suitability of the Lifetime ISA introduced 8 years ago.

What is a Lifetime ISA (LISA)?

To encourage saving for both property purchase and retirement, the Government launched the LISA in April 2017.

- Available for 18-39 year olds.

- All contributions must stop at age 40.

- LISAs are an extension of the ISA in that your savings grow tax free but with an extra 25% savings bonus added by the government.

- Maximum savings £4,000 pa and with a government bonus of £1,000 (25%), meaning total annual savings allowance of £5,000.

- Savings can be withdrawn tax free keeping all bonuses added and used towards a deposit to buy your first home (maximum purchase price £450,000) or be left until retirement age, currently age 55 (increasing to 57) and then drawn tax free too.

- Unauthorised withdrawals e.g., simply cashing in the LISA early without using towards a deposit for a property or in retirement means a 25% penalty is applied.

Findings by HMRC and included in the Treasury Report concluded that:

- Only 6% of eligible people have opened a LISA.

- 1 in 7 of ISA providers offer LISAs.

- Many LISA providers only offer the cash Lifetime ISA meaning it is not a suitable investment vehicle for this saving for retirement where longer term investment classes such as bonds and equities would be more suitable.

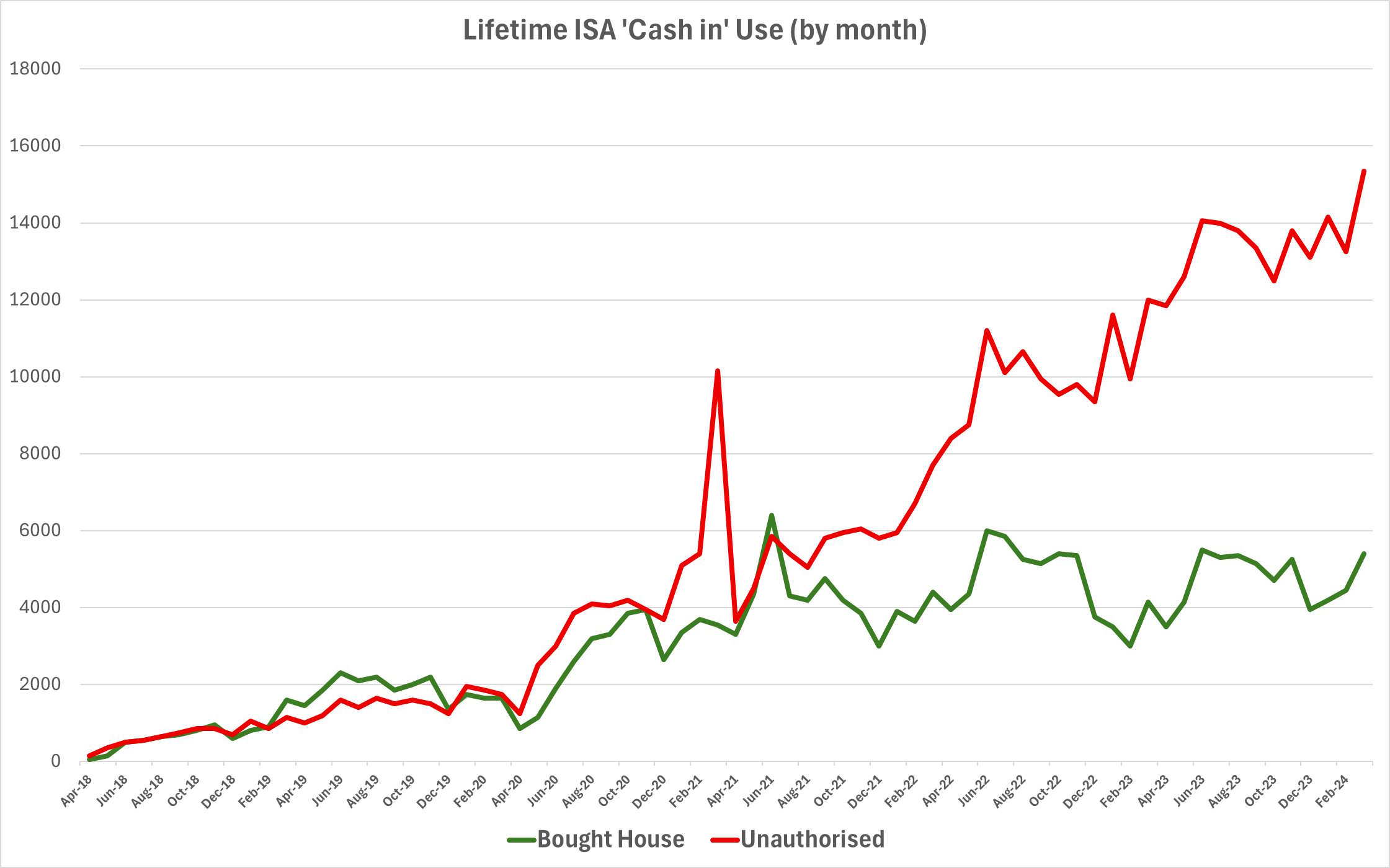

- Too many savers are people are cashing in early and not using for house purchase or retirement meaning an unauthorised withdrawal and incurring the 25% withdrawal charge, indicating that the LISA is not working as intended.

- The high rate of unauthorised withdrawals also indicates a lack of understanding of the withdrawal charge and is inflexible in that LISAs cannot adapt to an unforeseen change in circumstances.

- Saving for retirement with a Lifetime ISA is working well for self-employed people as it can adapt to house purchase or retirement but may not work so well for self employed or employees if they are 40% or 45% tax payers and many be better suited using workplace pensions.

- The Government is keen to support and encourage people onto the property ladder but given the pressure on public finances, the Government must carefully consider whether significant spending on the Lifetime ISA is the best way of achieving its policy objectives given the 25% bonus is set to cost the Government £600m ins 2027/28.

Comment

Using HMRC’s figures, we calculated that on average between April 2018 and March 2024, 60% of all LISA encashments were unauthorised resulting in a 25% penalty. In recent years, January 2023 to March 2024, this had risen to 74%.

We have already heard rumours that the Cash ISA allowance may be reduced from £20,000 pa to just £4,000 pa and now with this critical report on Lifetime ISAs, we expect significant changes from Chancellor Rachel Reeves in the Autumn Budget 2025.